Marketing

-

by Adam N. Rabinowitz and Walter Scott Monfort Click to download a PDF version of this publication. The United States Department of Agriculture (USDA) National Agricultural Statistics Service (NASS) released their Crop Production report on August 12, 2019. Their report forecasts 2019 harvested acres in Georgia at 590,000, down from 650,000 in 2018. The basis…

-

The original deadline to sign up for the Market Facilitation Program was January 15, 2019; however, the deadline will be extended for the number of business days USDA FSA offices were closed, once the government shutdown ends.

-

by Levi Russell A new publication entitled “Surviving the Farm Economy Downturn” is now available online free of charge. The publication provides a general farm economy outlook as well as discussions of topics such as risk reduction, cost control, alternative crops, livestock sales during drought, crop insurance, ARC and PLC payment forecasts, stress and suicide,…

Posted in: Beef Cattle, Cotton, Dairy, Finance, Horticulture, Management, Marketing, Peanuts, Policy, Poultry, Row Crops, Turfgrass, Vegetables -

by Levi A. Russell A couple of recently-released reports provide some interesting observations about the state of the beef industry and some good news for the long run as well. Beef Demand First, a few of my colleagues at Kansas State and Purdue Universities have written an extensive report on many drivers of beef demand.…

-

by Adam N. Rabinowitz The 2017 peanut harvest is well underway with over 70 percent of the Georgia crop dug and over 50 percent harvested. While Hurricane Irma negatively impacted the cotton crop, there was no widespread negative impact on peanuts. Both irrigated and dryland peanuts are looking good. Peanut yields in Georgia and the…

-

by Levi Russell Last week in Atlanta Extension economists, lenders, and ag media met in Atlanta to discuss the market and policy outlook for agricultural commodities in the Southeast in the coming year. UGA economists presented the outlook for peanuts, timber, turfgrass, the green industry, cotton, poultry, and hogs. All presentations are available here. Feel…

Posted in: Beef Cattle, Cotton, Dairy, Horticulture, Marketing, Peanuts, Policy, Poultry, Row Crops, Turfgrass -

I’ve been getting a lot of questions lately about opportunities for the US beef industry in China. Given the way these deals can go, I was hesitant to put a lot of faith in the possibility of re-opening this market (after 14 years). But today we received news that Greater Omaha Packing will be shipping…

-

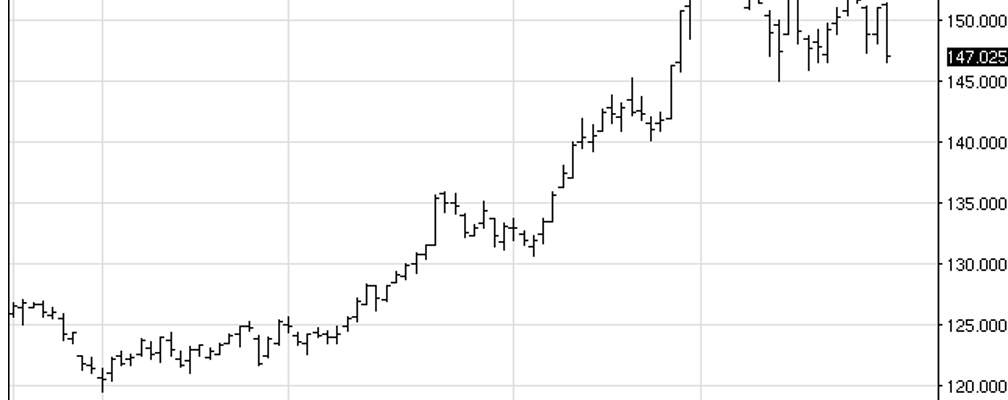

by Levi Russell The recent run-up in wholesale beef prices has sent cash and futures prices through the roof in the past few weeks. This provides an opportunity for producers with spring-calving herds to lock in a profit. For instance, right now producers can buy a put option on the September feeder contract at a…