Georgia farmers can produce a wide range of fruits, vegetables, nuts, pulses and grains with eight different USDA hardiness zones (6A-9B), a diverse geography and variable climate. While a substantial portion of what’s grown in Georgia is sold and distributed at the commodity level, there is still a vast range of produce available to consumers throughout the state via farmers markets, local distributors and retailers, or direct from the farm. For restaurateurs, small food businesses, agritourism operators, and destination managers, taking advantage of this agricultural bounty can play a significant role in adding value, differentiating from competitors, and creating a competitive edge.

Since the 1990’s, interest in local foods has increased significantly among chefs, food retailers, politicians, journalists, academics and the general public. To this day, there are still debates around what defines “local.” Even the USDA recognizes there is no singular definition for local or regional food, but recognizes in broad terms they are foods produced and sold to consumers within a certain distance or geographic boundary. The USDA’s Agriculture Marketing Service often uses the definition for local and regional foods as “the distance between product origin and point of sale is at most 400 miles, or both the final market and the product origin are within the same State, US territory, or Tribal land”. Whereas from a consumer perspective, research has shown they consider local to be food that is produced, processed, marketed and consumed within a geographically or politically circumscribed area.

The rise in popularity and significance of local food amongst consumers can be attributed to several factors, including a negative reaction to issues associated with a globalized and industrialized food systems (such as deforestation, land-use change, greenhouse gas emissions, etc.), and a positive movement that supports community and rural economic development. For hospitality and tourism, especially within the restaurant industry, local food has been one of the most consistently popular trends year over year—with a majority of consumers repeatedly stating they prefer to visit and recommend restaurants that use local ingredients over those that don’t. There is also a growing segment of travelers where local food plays a significant role in both their destination choice as well as their ultimate experience. Most importantly, over the last couple of decades, research has consistently shown that consumers not only value and prefer local food, they are also willing to pay a premium for it.

While meeting this consumer interest and demand for local food is crucial to restaurants and food business operators, there are several additional benefits that can be realized through the sourcing of local ingredients. In addition to environmental benefits such as lower carbon emissions in terms of transportation/distribution, storage, and packaging, sourcing locally can also help support independent and small farmers, establish positive community relationships, and keep money in a local economy. Other benefits include improved customer satisfaction, increased intention to revisit, generating good PR, and helping to create a memorable experience and a sense of place for visitors.

Another major benefit to sourcing ingredients locally is the overall enhanced quality, taste and freshness of the produce. For restaurant chefs, especially those in independent, small restaurants, as well as most upscale or fine dining restaurants, the quality and freshness of the menu ingredients—which directly impacts the way they taste, is of the utmost importance and is often the key component to creating a competitive advantage and differentiating from competitors.

However, despite all the benefits and advantages of sourcing local ingredients, it does not come without challenges. There can be several barriers that operators and food service businesses face when trying to procure ingredients locally. These can include, but are not limited to, inconsistencies in size, appearance, shape of produce; limited availability and limited quantity; inconvenient ordering or procurement processes; inadequate distribution; and variable costs. One of the most commonly reported barriers to sourcing local ingredients is a general lack of knowledge, information, or awareness about local sources. There can be a variety of reasons for this gap, but unless chefs and food purchasers actively seek out and research what local food is available, they often possess little familiarity with all the possible local ingredients, when they are in season, and how or where to get them. Likewise, businesses often believe that local products cost more, when, in fact, there is little evidence to support a significant difference in direct operator costs between sourcing local vs non-local ingredients. However, there can be potential indirect costs associated with sourcing locally, such as finding a reliable supplier and negotiating fulfillment contracts.

The purpose of this document is to reduce the knowledge gap about local produce in Georgia and serve as a resource for chefs, restaurateurs and small food businesses by providing a comprehensive inventory of the produce (fruit, vegetables, pulses, grains and herbs) grown in Georgia and when each is in season. The hope is food and beverage business operators will utilize this chart to better acquaint themselves with what is available from their local farms, in what quantities, and when. Armed with that knowledge, they can plan their menus or offerings around what will be in season, then connect with their local farms either directly or through farmer’s markets or local distributors to fulfill their needs. Beyond menu planning, this information can also help operators forecast labor needs, assist with budgeting, and can be incorporated into future marketing campaigns. Furthermore, beverage operations, such as breweries, wineries, and distilleries, can also factor this information into their production schedules, new product development, and marketing initiatives. By sourcing local, these operators can support their local economy, reduce their carbon imprint, and, by communicating their local offerings effectively to the public, they can capitalize on the growing consumer demand and willingness to pay a premium for locally sourced menu items.

Georgia Produce Seasonality Chart

Legend: A = Available, L = Limited Availability, Blank = Not Available.| Plant Name | Plant Type | Jan | Feb | Mar | Apr | May | Jun | Jul | Aug | Sep | Oct | Nov | Dec |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Apples ⁱⁱⁱ | Fruit | A | A | A | A | A | |||||||

| Arugula ⁱ | Veg | A | A | A | |||||||||

| Asparagus | Veg | A | A | A | |||||||||

| Basil ⁱ | Herb | A | A | A | A | A | L | L | |||||

| Beans (Green/ Hericot Vert) | Other | A | A | A | A | A | A | A | |||||

| Beans (Lima) | Veg | A | A | A | A | ||||||||

| Beets/ Beetroot | Veg | A | A | A | A | A | A | A | A | A | |||

| Blackberries | Fruit | A | A | A | |||||||||

| Blueberries | Fruit | A | A | A | A | ||||||||

| Bok Choy | Veg | A | A | A | A | A | A | A | A | A | |||

| Broccoli | Veg | A | A | A | A | A | A | A | A | ||||

| Brussels Sprouts | Veg | A | A | A | A | ||||||||

| Cabbage | Veg | A | A | A | A | A | A | A | A | ||||

| Cantaloupe (Melon) | Fruit | A | A | A | |||||||||

| Carrots | Veg | A | A | A | A | A | A | A | A | ||||

| Cauliflower | Veg | A | A | A | A | A | A | A | A | A | |||

| Celery (and Celery Root) | Veg | A | A | A | A | A | |||||||

| Chard | Veg | A | A | A | A | A | A | A | A | ||||

| Chives | Herb | A | A | A | A | A | A | A | A | A | A | A | A |

| Cilantro ⁱ | Herb | A | A | A | A | A | A | ||||||

| Citrus (Mandarin) | Fruit | A | L | A | A | A | |||||||

| Collard Greens | Veg | A | A | A | A | A | A | L | |||||

| Corn (Sweet) | Other | A | A | A | |||||||||

| Cucumbers | Veg | L | A | A | A | A | L | L | |||||

| Dill | Herb | A | A | A | A | A | A | A | |||||

| Edamame (Soy bean) | Veg | A | A | A | A | ||||||||

| Eggplant | Veg | A | A | A | A | A | |||||||

| Fennel ⁱⁱ | Herb | A | A | A | A | A | A | A | A | A | A | A | A |

| Figs | Fruit | A | A | ||||||||||

| Garlic ⁱⁱⁱ | Veg | A | A | A | A | A | A | ||||||

| Garlic Scapes/ Green Garlic | Veg | A | A | A | |||||||||

| Grapes (Muscadine) | Fruit | A | A | A | A | ||||||||

| Green Onions (Scallions) | Veg | A | A | A | A | A | |||||||

| Hibiscus | Fruit | A | A | ||||||||||

| Kale ⁱ | Veg | L | L | A | A | A | A | A | A | ||||

| Kohlrabi | Veg | A | A | A | A | A | |||||||

| Leeks | Veg | A | A | A | A | A | A | A | A | ||||

| Lettuce ⁱ | Veg | L | L | A | A | A | A | A | A | A | A | ||

| Lemongrass | Herb | ||||||||||||

| Maypop (Passion fruit) | Fruit | A | A | L | |||||||||

| Melons (other than cantaloupe) | Fruit | L | A | A | A | A | L | ||||||

| Mint | Herb | A | A | A | A | A | A | A | |||||

| Mushrooms (cultivated), year-round | Other | A | A | A | A | A | A | A | A | A | A | A | A |

| Mustard Greens | Veg | A | A | A | A | A | A | A | A | A | |||

| Okra | Veg | A | A | A | A | A | A | ||||||

| Olives | Fruit | A | A | A | |||||||||

| Onions (sweet, Vidalia) ⁱⁱⁱ | Veg | A | A | A | A | A | A | L | |||||

| Oregano | Herb | A | A | A | A | A | A | L | |||||

| Parsley ⁱⁱ | Herb | L | L | A | A | A | A | A | A | A | A | A | A |

| Parsnips | Veg | A | A | A | |||||||||

| Peaches | Fruit | A | A | A | A | ||||||||

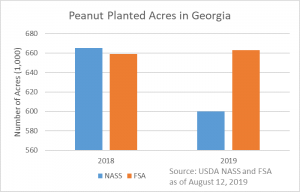

| Peanuts | Other | A | A | A | A | ||||||||

| Pears | Fruit | A | A | A | A | ||||||||

| Peas (field, cowpeas, black-eyed) | Other | A | A | A | A | A | A | ||||||

| Peas/Pea Pods | Other | A | A | A | A | ||||||||

| Pecans | Other | A | A | A | A | ||||||||

| Peppers (sweet and hot) | Veg | L | A | A | A | A | A | L | |||||

| Persimmons | Fruit | A | A | A | |||||||||

| Plums | Fruit | L | L | A | A | A | |||||||

| Potatoes (Irish) ⁱⁱⁱ | Veg | A | A | A | A | L | |||||||

| Potatoes (Sweet) | Veg | A | A | A | A | A | A | A | |||||

| Pumpkin | Veg | A | A | A | |||||||||

| Radishes | Veg | A | A | A | A | ||||||||

| Raspberry | Fruit | A | A | ||||||||||

| Rosemary ⁱⁱ | Herb | A | A | A | A | A | A | A | A | A | A | A | A |

| Sage ⁱⁱ | Herb | A | A | A | A | A | A | A | A | A | A | A | A |

| Sorrel | Herb | A | A | A | A | A | A | A | |||||

| Spinach | Veg | A | A | A | A | A | A | A | |||||

| Squash (summer; including zucchini) | Veg | A | A | A | A | A | A | A | |||||

| Squash (winter) | Veg | A | A | A | A | A | |||||||

| Strawberry | Fruit | A | A | A | |||||||||

| Tarragon | Herb | A | A | A | A | A | L | ||||||

| Thyme ⁱⁱ | Herb | A | A | A | A | A | A | A | A | A | A | A | A |

| Tomatoes | Fruit | L | A | A | A | A | A | L | |||||

| Turnips | Veg | L | L | A | A | A | A | A | |||||

| Watercress ⁱ | Herb | A | A | A | |||||||||

| Watermelon | Fruit | A | A | A | A |

The Georgia Produce Seasonality Chart is created by Dr. Daniel Remar – Assistant Professor of Hospitality and Food Industry Management at the University of Georgia College of Agricultural and Environmental Sciences.

Notes

- Georgia has 8 different USDA hardiness zones, so which and when produce is available varies by region.

- ⁱ can be grown in controlled environment year-round

- ⁱⁱ can be harvested perennially

- ⁱⁱⁱ extended availability from storage

Sources

Bacig, M., & Young, C. A. (2019). The halo effect created for restaurants that source food locally. Journal of Foodservice Business Research, 22(3), 209-238.

Björk, P., & Kauppinen-Räisänen, H. (2016). Local food: a source for destination attraction. International Journal of Contemporary Hospitality Management, 28(1), 177-194.

Campbell, J., DiPietro, R. B., & Remar, D. (2014). Local foods in a university setting: Price consciousness, product involvement, price/quality inference and consumer’s willingness-to-pay. International Journal of Hospitality Management, 42, 39-49.

Choe, J. Y. J., & Kim, S. S. (2018). Effects of tourists’ local food consumption value on attitude, food destination image, and behavioral intention. International Journal of Hospitality Management, 71, 1-10.

Curtis, K. R., & Cowee, M. W. (2009). Direct marketing local food to chefs: Chef preferences and perceived obstacles. Journal of Food Distribution Research, 40(2), 26-36.

Duarte Alonso, A., & O’Neill, M. (2010). Small hospitality enterprises and local produce: a case study. British Food Journal, 112(11), 1175-1189.

Enthoven, L., & Van den Broeck, G. (2021). Local food systems: Reviewing two decades of research. Agricultural Systems, 193, 103226.

Feldmann, C., & Hamm, U. (2015). Consumers’ perceptions and preferences for local food: A review. Food Quality and Preference, 40, 152-164.

Huang, Y., & Hall, C. M. (2023). Locality in the promoted sustainability practices of Michelin-Starred restaurants. Sustainability, 15(4), 3672.

Lang, M., & Lemmerer, A. (2019). How and why restaurant patrons value locally sourced foods and ingredients. International Journal of Hospitality Management, 77, 76-88.

Remar, D., Campbell, J., & DiPietro, R. B. (2016). The impact of local food marketing on purchase decision and willingness to pay in a foodservice setting. Journal of Foodservice Business Research, 19(1), 89-108.

Roy, H. (2024). Connecting farmers’ markets to foodservice businesses: A qualitative exploration of restaurants’ perceived benefits and challenges of purchasing food locally. International Journal of Hospitality & Tourism Administration, 25(3), 602-637.

Sharma, A., Gregoire, M. B., & Strohbehn, C. (2009). Assessing costs of using local foods in independent restaurants. Journal of Foodservice Business Research, 12(1), 55-71.

Tsai, C. T. (2016). Memorable tourist experiences and place attachment when consuming local food. International Journal of Tourism Research, 18(6), 536-548.